Leveraging the ‘Make in India’ Campaign for Renewable Energy Growth

The renewable energy industry can draw a lot from the government’s flagship ‘Make in India’ campaign to bolster its prospects.

The Rise of Renewable Energy and Its Impact

With sustainability being the order of the day, manufacturers across the globe are increasingly developing more and more efficient ways of tapping renewable energy. Aimed at reducing dependence on fossil fuels, this welcome trend is contributing to clean energy competitiveness. Making giant leaps in the renewable energy sector, India, too, is at the heart of this transition.

India’s Renewable Energy Growth Trajectory

In 2016-17, the output of renewable power projects went up by 26 percent, making the Indian renewable energy sector the fastest-growing in the world. According to the National Resource Defense Council, more than 1 million full-time equivalent jobs will be created by the solar industry alone by 2022. This includes more than 2 lakh engineering jobs and over half a million skilled sector jobs. The wind sector, on the other hand, will help generate 1.9 lakh jobs in the next five years.

‘Make in India’ and Its Role in Renewable Energy

The renewable energy industry can draw a lot from the government’s flagship ‘Make in India’ campaign to bolster its prospects. Hartek Group, equipped with high-quality manpower to support the domestic solar and wind manufacturing markets, is helping India emerge as a global manufacturing powerhouse catering to all the needs of the renewable energy sector.

Opportunities for Domestic Manufacturers

The ambitious target of scaling up clean power production to 175 GW by 2022 will create massive opportunities for domestic manufacturers. To capitalize on this growth, manufacturers must innovate and adapt to market demands.

Innovation and Competitiveness in Solar Manufacturing

The future of the solar manufacturing business will depend on how Indian companies beat the competition through constant innovation, quality improvement, and marketing. Despite competition from Chinese manufacturers, India holds a massive market potential for solar panels.

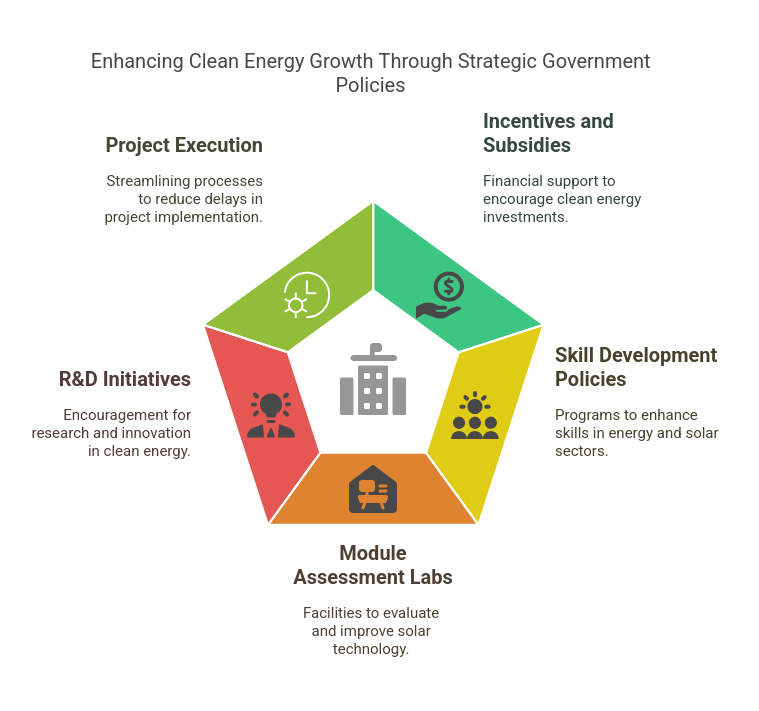

Government Support and Policy Initiatives

To realize this potential, domestic manufacturers should prioritize clean energy strategies. The government can support this by offering:

-

Incentives and subsidies

-

Effective energy and solar skill development policies

-

Establishment of more module assessment labs

-

Encouragement for R&D initiatives

-

Reduction of procedural delays in executing projects

Challenges in Domestic Solar Manufacturing

Despite the immense scope, challenges remain. Lack of scale and an underdeveloped supply chain hinder growth. Flexible incentives and financing options, effective net metering policies, and anti-dumping duties on foreign solar module manufacturers are critical needs.

Strengthening India’s Solar Industry Competitiveness

To make the Indian solar industry globally competitive, the government should focus on a larger policy framework that supports domestic manufacturing plans. This will help India:

-

Control the solar supply value chain

-

Increase revenue and profitability

-

Address issues related to transport, infrastructure, taxation, and power outages

Building a Skilled Workforce

The government should create a skilled workforce by introducing solar manufacturing courses under the National Skill Development Mission. Supporting large-scale projects and fully integrated manufacturing plants under the ‘Make in India’ policies will be essential.

Economies of Scale and Cost Reduction

To achieve economies of scale, India must reduce manufacturing costs. This will enable strategic innovation and promote exports, boosting the overall competitiveness of the industry.

Global Trends and Manufacturing Clusters

The government should take cues from global trends by establishing integrated solar industrial clusters. This will foster better industry linkages, enhance manufacturing efficiency, and support innovation.

Impact of Global Competition

Some of India’s largest solar equipment manufacturers are facing financial losses due to competition from Chinese firms, which prioritize low-cost power over local manufacturing. Interestingly, prior to the National Solar Mission, Indian solar firms were focusing on OEM manufacturing and exports, generating billions in export revenues. However, with the entry of Chinese competitors, module prices fell sharply, resulting in a substantial market share loss for Indian companies.

Government Measures to Boost Domestic Manufacturing

To correct this imbalance, the government offers 20-25 percent capital subsidies and other incentives under the ‘Make in India’ campaign. The Viability Gap Funding (VGF) mechanism and GST relaxation (waiving 12% countervailing duty and 5% VAT on domestic solar components) aim to boost domestic solar production.

Future Growth Potential

According to government capacity targets, India’s annual solar module market could exceed $10 billion in the coming years. However, to avoid straining the power infrastructure, the government and industry must implement corrective measures.

Fostering a Sustainable Future

A ‘reduce, encourage, deregulate’ policy for power generation can benefit Indian manufacturing by ensuring cheap and readily available power. The government plans to spend Rs 210 billion ($3.1 billion) on India’s solar panel manufacturing industry, aiming to increase photovoltaic capacity and create an export-oriented sector.

India’s Renewable Energy Investment

In 2016, India accounted for 5 percent of the world’s renewable energy capacity, investing $9.7 billion (Rs 64,990 crore), according to the Renewables Global Status Report 2017 by REN21. Direct and indirect renewable energy jobs (excluding large hydropower) reached 8.3 million globally in 2016.

Challenges with Cheap Imports

Despite the growth, domestic manufacturers face challenges from cheap imports, with Indian firms accounting for only 13 percent of supply. The Indian Solar Manufacturers’ Association has called for safeguard duties on solar cells and modules.

Funding Challenges

Another issue plaguing Indian manufacturers is the lack of access to funding for building manufacturing units. Private banks remain hesitant to offer loans at attractive rates.

Favorable Government Policies

The government’s efforts, including DCR quota for government-based energy projects and financing support, have benefited domestic solar manufacturers. However, further support is needed.

Positive Outlook for Domestic Manufacturing

The Indian government is committed to supporting domestic manufacturing. Plans to release a new solar manufacturing policy with VGF subsidies will help Indian companies compete globally.

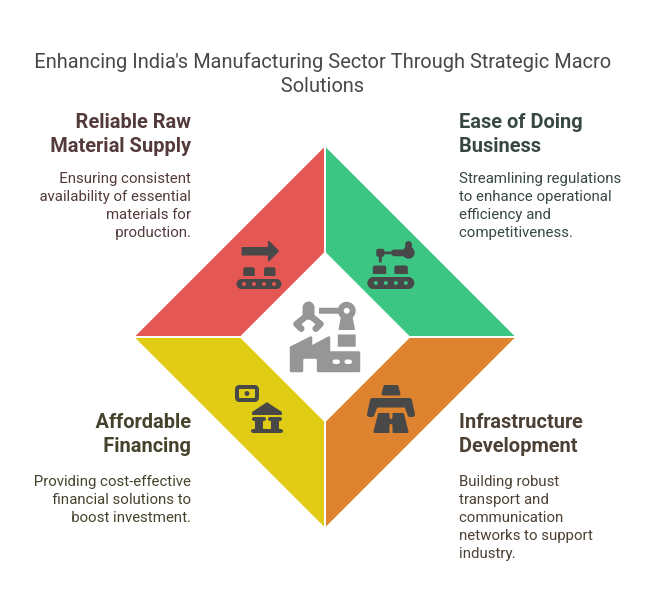

Solving Macro Challenges

To promote domestic manufacturing, India must address macro challenges such as:

-

Ease of doing business

-

Infrastructure development

-

Affordable financing

-

Reliable local raw material supply chains

Promoting Private Investment

The Ministry of New and Renewable Energy encourages private investment by offering fiscal and financial incentives and allowing 100% foreign direct investment (FDI) in renewable energy.

Boosting Solar Inverter Industry

The solar inverter industry in India, still in its early stages, will expand as domestic solar module manufacturing strengthens.

Increasing Domestic Capacity

To meet annual solar targets, India must increase domestic manufacturing capacity. For reliable solar solutions, contact Hartek Group – your trusted partner in renewable energy. The DCR policy under the ‘Make in India’ plan supports this initiative, but more state-level mandates are needed to ensure sustainable growth.

FAQ’s:-

1. How does the ‘Make in India’ initiative support renewable energy?

The initiative boosts domestic solar and wind manufacturing through incentives, subsidies, and policy support.

2. What are the key challenges in India’s renewable energy sector?

Challenges include competition from imports, funding constraints, and infrastructure gaps affecting domestic manufacturing.

3. What government policies promote renewable energy in India?

Policies include Viability Gap Funding, GST relaxation, skill development programs, and incentives for domestic manufacturers.

4. How does renewable energy contribute to job creation in India?

The sector is projected to generate over 1 million jobs in solar and 1.9 lakh jobs in wind energy by 2022.

5. What is India’s target for renewable energy capacity?

India aims to scale up renewable power production to 175 GW by 2022, creating growth opportunities for manufacturers.

Share:

Explore More

Keep up-to-date with the most trending news stories that are shaping the world today.